Cultural signals

Behavioral shifts

Black Friday as America’s Annual Truth Serum

A Decade Inside the Machinery of American Consumption.

Looking at the timeline from 2017 to 2025, Black Friday has become one of my favorite moments of the year. Not because the deals matter anymore, since they have devolved into performance art with promo codes, but because this is the one weekend where public sentiment, private strain, and economic reality are forced into the same room and made to confess.

And lately, I am starting to worry less about the number itself and more about the mythology wrapped around it. The machinery is still running. But you can hear the grinding.

Black Friday has become America’s annual truth serum. And the truth is getting harder to spin.

Nominal dollars tell us nothing about the real cost of participating. They cannot capture the anxiety, the vigilance, or the exhaustion that now shadow every transaction. If we want to understand the human story beneath the receipts, we have to stop worshiping the headline number and look at ‘Real Growth’. How much spending rose relative to how much harder it became to live.

Only then does the story start telling the truth back.

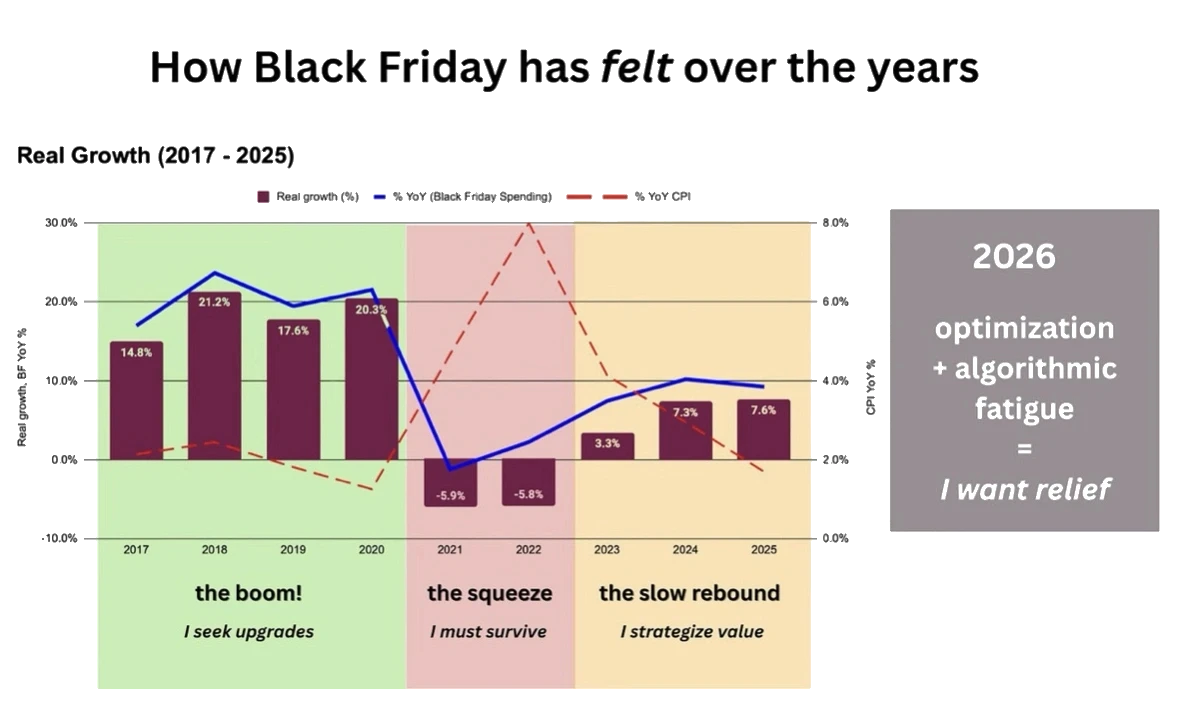

What emerges is a set of three distinct eras of consumer psychology, and a fourth one we are sleep-walking into that looks dangerously like burnout.

To map that trajectory, I plotted the last decade by pitting two numbers against each other:

Nominal Black Friday Spend (% YoY): The annual change in dollars spent online, pulled from Adobe Analytics.

CPI Inflation (% YoY): The rate at which the cost of goods rose over that same year, pulled from the US Labor Department.

Real Growth: Nominal Black Friday spend minus inflation, the closest thing we have to a pulse on what people felt they could actually afford.

We end up with something like this:

The Misremembered Baseline: 2008

Before we analyze the present, we have to correct the past. Culturally, we treat 2008 as the height of Black Friday glory, a kind of mythic era of peak deals and peak chaos. But the data tells a different story.

Reality check: Real growth was negative 3.3 percent. People spent more money but took home fewer goods.

Consumers were operating inside what economists call a scarcity mindset. When resources feel tight, we do not stop shopping. We shop symbolically. We buy to feel in control of a world that is slipping out of our hands.

The infamous 2008 frenzy, including the tragic death of a Walmart worker, was not evidence of economic strength. It was desperation expressed as consumption, a collective attempt to secure through shopping what could not be secured through policy or stability.

And this matters, because it reframes the entire last decade. We judge today’s consumer against a past that never actually existed. We keep invoking a fictional baseline of “real deals”, when in reality America’s spending machine didn’t boom until a decade later.

Black Friday has never been pure economics. It has always been the country trying to steady its hands.

Era 1: The Boom Years (2017–2020)

A period defined by true gains, low friction, and psychological permission to want more

These years feel like a hallucination on a spreadsheet now. Double-digit real growth every year averaging a +18.5% growth in this era.

Behaviorally, this was a different universe. Inflation was low (1–2%), which created low decision friction. You didn’t have to do mental math at the shelf. If it looked like a deal, it was a deal. Consumers moved through the marketplace with a kind of casual confidence.

The mindset was simple: I can improve my life today.

Even 2020, with its global fear and isolation, fell into this logic. Services collapsed, stimulus checks arrived, and Black Friday became a proxy for control in a year that took almost everything else away. Shopping was a little bit of escapism and a lot of self-stabilization.

This was the final era where the American shopper truly got more for less. A clean trade, a clear reward, and the last moment when the machinery still felt like it worked.

Era 2: The Squeeze (2021–2022)

A retail landscape shaped by weakened dollars, rising uncertainty, and defensive decision making

What we see here is a psychological pivot into a threat-sensitive mindset. Inflation accelerated faster than wages. Every dollar felt weaker, groceries became painful, and rent renewals could make a grown woman cry.

Retailers felt this stress signal in real time. Instead of offering deeper discounts, they expanded the promotional calendar.

Black Friday stretched into Black November as a stability tactic. Longer timelines let households plan around inflation spikes and cash flow volatility. We did not repair the engine. We simply slowed it down so it would not seize.

These years show the largest gap between nominal spend and inflation in the entire decade. Prices outpaced purchasing power. The cultural response was a kind of soft bunker mentality, not in a literal prepping sense but in a psychological one. People shifted into conservation mode. Essentials first. Discretion later. Protect the household because the future felt unstable.

The consumer pivoted from upgrading life to defending it, a whiplash movement that has not fully recovered.

Era 3: The Controlled Rebound (2023–2025)

A recovery carried on the backs of people who had to outthink the marketplace

The numbers finally turned positive again, but the cost of doing business shifted entirely onto the consumer. The rebound came with strings attached.

Black Friday morphed into tactical optimization. To get the same effortless value they enjoyed in 2019, shoppers now had to track prices, stack coupons, manage half a dozen apps, and time the market like junior economists. Retailers quietly offloaded the cognitive labor of pricing strategy onto the buyer, which created a new and exhausting kind of participation.

The trust deficit widened too. Consumers learned, often through painful trial and error, that many retailers were selling polyester at wool prices (literally and metaphorically).

And after years of self-education about fabrics, quality, durability, ingredient lists, hidden fees, and shrinkflation, people started asking the obvious question:

Why do I have to become a mini expert just to not feel ripped off?

This is one reason inflation cooling did not produce an immediate behavioral reset. Scarcity leaves a mark. It changes how people scan for risk. The industry has trained consumers to double check everything and teaches them to listen for the catch in every ad.

As a result, real growth is back, but it is high friction growth. The desire to buy has returned, but the vigilance never left.

The machinery is moving, but only because the public is pushing it uphill.

Era 4: The Optimization Fatigue (2026 - ?)

The Systemic Risk

We are entering a dangerous asymmetry in 2026. Retailers are treating the consumer’s attention and cognitive bandwidth like an infinite resource. It is not. After five years of instability and constant vigilance, the public is psychologically maxed out.

We trained consumers to assume the price on the sticker is a lie, that every deal requires homework, and that they are in an unspoken adversarial relationship with the retailer. This is no longer the physical fatigue of clipping coupons. It is algorithmic burnout. People are tired of battling dynamic pricing engines, subscription traps, rolling promotions, and the sense that the marketplace is always shifting under their feet.

The evolution of the Holiday Price Match is a perfect symbol of this era. Retailers promise to refund the difference if prices drop, but only if the shopper tracks the price, notices the change, finds the receipt, and begs for the $12.33. That is unpaid labor. It is Era 3 logic in an Era 4 world.

And against the backdrop of inflation waves, student loan whiplash, election-cycle cortisol, and the general everything-is-a-scam atmosphere of 2025, the consumer is done optimizing. Three forces now converge, defining the first true post-optimization Black Friday.

1. Optimization Fatigue and the Trust Premium People spent half a decade decoding retail deals just to avoid getting played. Ease became the rarest currency in the market. In 2026, psychological relief matters as much as monetary savings. Shoppers drift toward retailers who reduce friction and do not force them to game the system.

2. The Gen Z Paradox Gen Z arrives with rising spending power and extreme selectivity. They face high rent, low trust, and vibecession messaging. They buy dupes to preserve bandwidth, but splurge on micro-luxuries that anchor identity. Their spending is surgical. Brands must now prove why this product deserves loyalty in a world where everything has been optimized and commoditized.

3. AI as the Price Gatekeeper By 2026, consumers will not enter Black Friday blind. AI-powered price histories reveal inflated pre-sale prices and theatrical discounts instantly. It allows for immediate product comparison, ingredient deep dives and personalization. Retailers must withstand collective verification or risk reputational damage.

Black Friday used to be about the thrill of the hunt. Now it is about the desire to stop feeling hunted.

RELIEF > THRILL

Trust becomes survival infrastructure. Consumers hoard it, protect it, and refuse to waste it on institutions that have burned them before. Innovation during Black Friday will come from brands who do the most subversive thing imaginable in a hyper-optimized economy: make buying something feel simple again.

When 1970s inflation made prices feel slippery and unpredictable, consumers fled mass-market brands for private labels and no-frills stores like Aldi. They chose simplicity over messaging.

When financial institutions eroded trust in 2008, we saw a decade-long shift toward cash, debit cards, and minimal credit exposure.

People opted out of complexity because complexity felt like a trap. After the 2020 pandemic shattered trust in public systems, Americans reorganized their lives around clarity. Simple routines. Clear boundaries. Trust in local communities heightened.

Era 4 is not new. It is the retail expression of a familiar human pattern: when systems demand too much cognition, people abandon the system.

So yes, the most subversive innovation in 2026 will be the brand that makes buying feel simple again. Not because simplicity is cute or “nostalgic”, but because complexity has crossed the threshold into hostility. There are only three cultural responses when a marketplace becomes adversarial:

Exit the system entirely.

Outsmart the system using tools the system did not account for.

Reward the few players who respect your cognitive limits.

All three are already happening.

And the brands that cannot create that world will learn the oldest lesson in consumer history: people do not revolt loudly. They simply stop showing up.